Present, Then Displaced

A shopper asks ChatGPT which serum to buy. She asks Gemini for a comparison. She asks Perplexity to settle it. By the time she reaches the retailer, the decision is already made, inside a model she cannot see, against competitors she did not choose to be ranked against. We measured what happens inside that conversation across 28 beauty and cosmetics brands. Most of them lose.

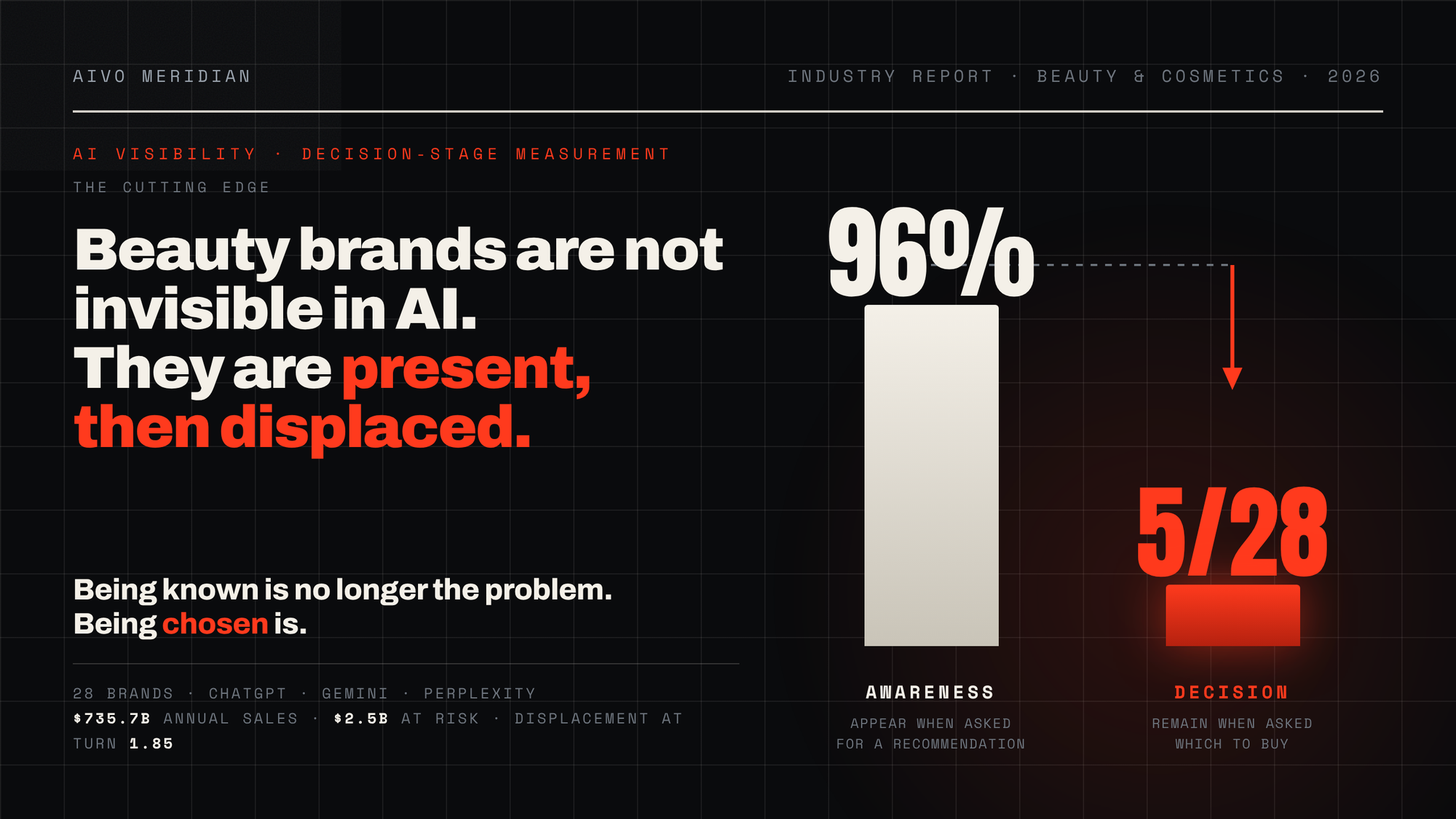

The problem is not visibility

Beauty brands are not invisible in AI. 96 percent of the brands we measured appear at the awareness stage, the moment a shopper first raises the category. That is the number every brand wants to hear and the number that hides the real story.

Five of 28 are still present at the decision turn, the moment the shopper stops browsing and asks which product to actually buy. The journey from "tell me about retinol serums" to "so which one should I get" is short, and it is where the brand disappears. Awareness is solved. The work has moved downstream, to the turn that ends in a purchase, and almost nobody is winning it.

Displacement is fast

The average brand is displaced at turn 1.85. More than half of all displacements happen at the very first follow-up. By the time a shopper has typed her second message, the brand has already lost in 55 percent of the cases where it loses at all.

That is a brutal window. A brand has fewer than two conversational turns to establish itself before the model moves on to a competitor. Most brand strategy is built for a funnel that gave you weeks. This one gives you a sentence.

The mechanism is comparative

Of every displacement we recorded, 84 percent were comparative. The pattern is consistent across the corpus and it is worth understanding precisely, because it is the whole game.

The model takes the shopper's request and reframes it as a structured evaluation. It grades each brand on four axes: effectiveness, value, reputation and accessibility. Then it selects the brand with the broadest, most consistent evidence across all four. It does not reward a brand that is brilliant on one axis and thin on another. It takes the lower bound. A brand with an extraordinary efficacy story and a weak reputation footprint loses to a brand that is merely solid on both.

This is the part that breaks intuition. The model is not running a beauty pageant. It is running a due diligence check, and it penalizes gaps far more than it rewards peaks.

Mass is beating prestige

The brands winning the decision turn are not the brands with the largest marketing budgets or the deepest heritage. Two mass-market brands account for more than half of every decision-turn win across the entire cohort. Prestige and heritage brands consistently lose the comparative evaluation despite stronger recognition.

The reason follows directly from the mechanism. The model does not weight brand equity the way a human shopper does. It weights evidence density. Mass brands tend to carry enormous, structured, consistent evidence across reviews, retail listings and editorial coverage, which is exactly the diet the model reasons over. Prestige concentrates its evidence inside brand-controlled channels that the model barely reads.

Where prestige does survive, it survives narrowly, as a named hero SKU rather than as a parent brand. The single iconic product holds where the wider range gets displaced. The model treats that hero as a distinct, well-evidenced entity and treats the rest of the range as noise.

Most of the evidence is invisible to the brand

We ran a deep catalogue audit of one hero brand's 951 SKUs across 242 unique source URLs the models drew on. The single largest category of cited source, at 39.7 percent, was material the brand cannot see and is not measuring at all. Editorial sources like Vogue, Allure and Byrdie made up another 27 percent. Brand-owned content accounted for roughly a fifth.

Read that against how brands actually invest. Product information management systems, the structured backbone most brands rely on to control how their products are described, address around 2 percent of the source diet driving the model's reasoning. The other 98 percent sits in editorial, retailer and community sources the brand does not own and is not watching. Closing the gap is not a data-feed exercise. It is an intervention in layers most beauty marketing has never had to manage.

The three platforms are not the same brand

Treating AI search as one surface is a mistake. The three assistants behave differently enough that a single strategy fails on at least one of them.

ChatGPT is the aggressive displacer. It drops brands the fastest, with a median displacement at the first turn. The upside is coherence. What you see when you test it is close to what it actually does internally, which makes it the strictest but most honest examiner. Optimize for it first.

Gemini is the dangerous one. In the specified queries a shopper actually types, the average brand appeared in 42.9 percent of probe turns. In the longer agentic reasoning the model runs internally, the same brand appeared in 84.7 percent. That is a 41.9 point gap between what casual testing shows and what is really happening. Anyone judging Gemini by typing a few prompts and watching for their name is measuring almost nothing.

Perplexity is the patient one. It holds named brands in scope longer, has the highest average presence, and diverges least between what it shows and what it does. Its citation-grounded architecture keeps brands in the conversation rather than reasoning ahead of them.

What it costs

Across the 28 brands, representing 735.7 billion dollars in annual sales, the revenue currently at risk to AI displacement is 2.5 billion dollars. That figure combines the consistency deficits, the displacement timing and the category exposure into a single number. It is not a forecast for 2027. It is attributable revenue moving through these conversations today, while the brands losing it are still reporting that they appear in AI search.

What it means

Five shifts follow from the data, and none of them are optional.

Measure the agentic surface, not just the one you can see. The Gemini gap proves that ad-hoc testing produces a number that is close to meaningless on the platform where it matters most.

Win the decision turn, not the awareness turn. Investment optimized for "do they know us" is solving a problem that is already solved. The open problem is "do they recommend us when asked to choose."

Build evidence across all four axes, because the model takes the lower bound. Find your weakest axis and close it before you extend your strongest.

Treat editorial and retailer evidence as primary. It carries more weight in the model's reasoning than brand-owned content does, and most brands still treat it as an afterthought.

Make your claims consistent across regions and retailers. When the same product says different things on different surfaces, the model reads the inconsistency as a confidence signal and downgrades the entire brand.

The line under all of it

Being known is no longer the problem. Being chosen is. The brands that understand this early will treat AI recommendation as a measurable surface with its own mechanics, the way they once learned to treat search. The brands that do not will keep reading last-click analytics and wondering why the funnel feels different.

The full study, The State of Beauty and Cosmetics AI Visibility 2026, measured all 28 brands by sub-category, platform and decision-turn outcome. It is available on request (from: tim@aivostandard.org), along with a confidential brand-level audit that shows exactly where a single brand sits in the cohort.

If you want to know where your brand is being chosen and where it is quietly being displaced, that is the place to start: AIVO Meridian