Search Marries Content. The Babies Aren't Being Delivered.

Three DXP deals in sixty days have wired AI visibility into the content stack. What none of them have wired in is whether brands are actually being chosen.

In April, Adobe paid $1.9 billion for Semrush. On June 9, Sitecore acquired Scrunch for $225 million. On June 10 — less than thirty-six hours later — Optimizely launched a full Answer Engine Optimization platform anchored by a strategic partnership with Conductor.

Three of the four largest enterprise Digital Experience Platforms have decided, in roughly sixty days, that AEO is no longer a category they can leave to point solutions. The fourth, Salesforce, is busy digesting Contentful. The DXP layer has made up its mind: in the AI-mediated web, you cannot sell content management without selling AI visibility alongside it.

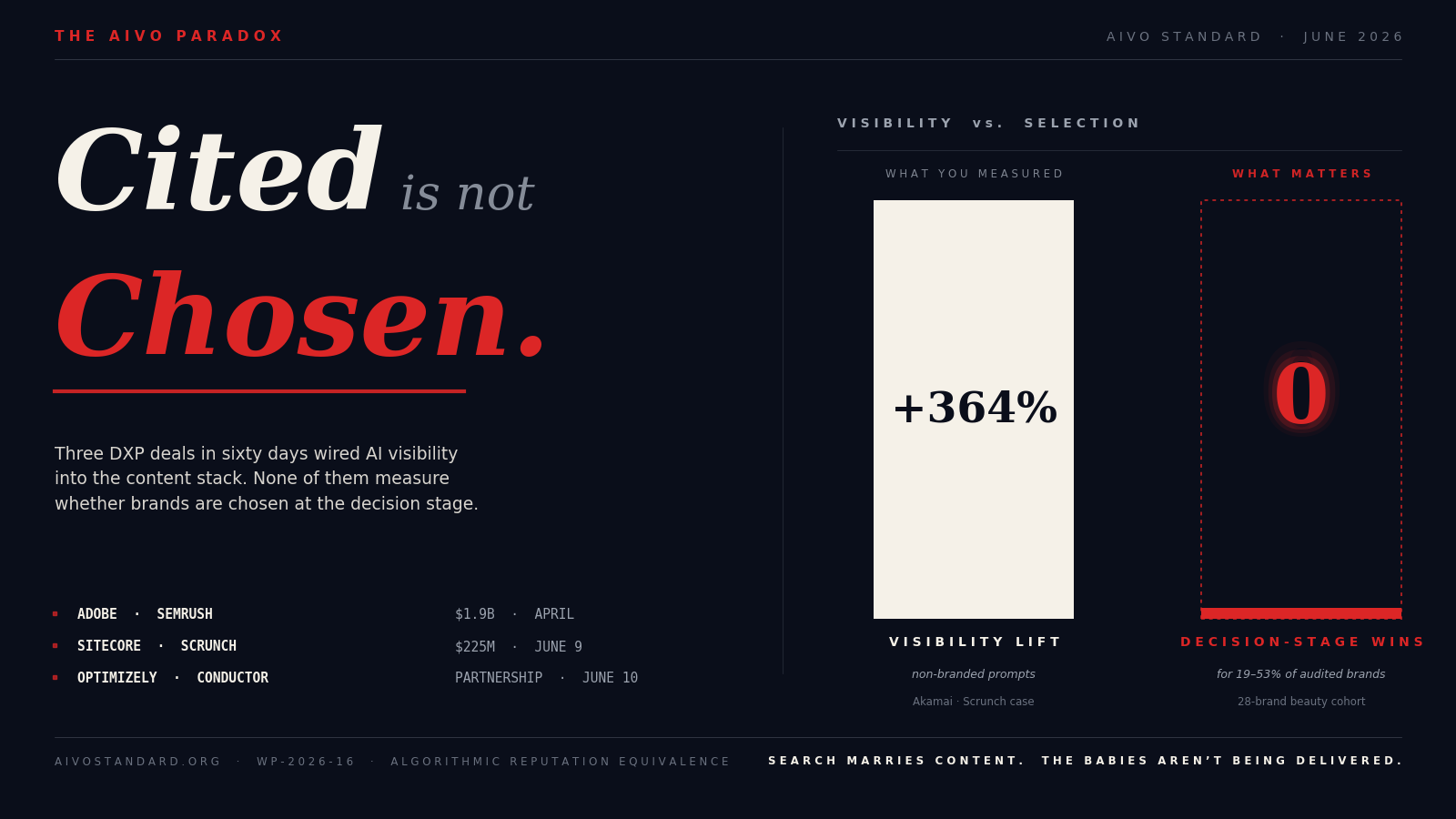

The shape of these deals is remarkably consistent. In each case, a content-and-experience platform has paired itself with a tool that detects AI agents, optimizes pages for retrieval, and reports on citation activity. The Sitecore/Scrunch announcement showcased a 364% lift in non-branded visibility for Akamai. The Optimizely/Conductor launch promises "Agent Visibility Analytics" using log-level data to classify bot intent. Adobe brings Semrush's twenty-year search-data heritage into the Experience Cloud.

The pattern is unambiguous. Search is getting married to content.

The honeymoon is producing press releases. The babies — the actual commercial outcomes brands need from AI-mediated discovery — are not yet being delivered.

What These Deals Actually Wire Together

Strip away the announcement language and each of these transactions does the same three things. They detect AI bot traffic arriving at a brand's properties. They serve those bots a more retrievable version of approved content. And they monitor whether the brand is being cited, mentioned, or referenced inside answer engines like ChatGPT, Gemini, and Perplexity.

This is necessary work. AI agents now generate the majority of HTTP requests on the open web — Cloudflare's Radar dashboard crossed that threshold earlier this year, eighteen months ahead of CEO Matthew Prince's own forecast. Brands whose CMS cannot serve machine-readable content are functionally invisible to the systems that increasingly mediate consumer discovery. The DXPs are right to act, and right to act quickly.

Necessary, however, is not sufficient.

What the DXP/AEO consolidation wave does not do — what it has not, as a category, even started doing — is measure what happens after a brand is retrieved. It measures whether you were seen. It does not measure whether you were chosen.

Cited Is Not Chosen

In a public audit we published last month — State of Beauty and Cosmetics AI Visibility 2026, covering 28 brands with $735.7 billion in aggregate revenue — between 19% and 53% of brands achieved zero decision-stage wins despite regular citation visibility in answer engines. The same brands appeared in upstream reasoning turns. They were retrieved. They were cited. They were not chosen.

We call this the AIVO Paradox, and it is the single most uncomfortable number in the category. It says, in plain terms, that the visibility metrics the DXP/AEO wave is consolidating around are measuring the wrong commercial endpoint. A 364% increase in non-branded visibility is a real and measurable outcome. It is also, on its own, not a revenue number. It is a prerequisite to a revenue number, and the gap between those two things is where most enterprise AI-discovery budgets are about to be lost.

The reasoning chain that produces an answer in ChatGPT or Gemini or Perplexity does not stop at retrieval. It continues through comparative evaluation, intent matching, prompt-phrasing variation, and a final selection turn. Brands can be present in turn one and gone by turn three. Brands can survive intact under one phrasing and disappear under a paraphrase. None of the tools consolidated in the last sixty days measure any of this. They were not built to.

What CMOs Will Ask in 2027 Budget Cycles

The current generation of AEO products is being sold to enterprise marketers on the implied promise that visibility equals commercial outcome. That promise will not be tested in a research paper. It will be tested in the budget conversation that begins roughly nine months from now.

A CMO who has just spent the back half of 2026 stitching Semrush into Adobe Experience Cloud, or Scrunch into Sitecore Content Hub, or Conductor into Optimizely, is going to walk into a Q4 2026 board meeting and be asked a simple question: Did revenue move?

The honest answer, if the only measurement tooling in the stack is visibility-based, will be: We don't know. The brand is more visible. Bots are retrieving the content. Citation counts have improved. Whether any of that converted into selection at the decision stage — whether the agentic shopper, the assisted researcher, the LLM-mediated buyer actually chose this brand over a competitor — is not a question the current stack can answer.

This is the gap. It will not stay open for long.

The Next Layer

If the last sixty days have taught the DXP category anything, it is that the M&A logic in AI-mediated discovery is moving faster than the buying cycle of the brands consuming it. Visibility tools went from standalone category to acquired feature in roughly eighteen months. Conductor, founded in 2010, took fifteen years to become an Optimizely partner; Scrunch, founded in 2023, took two and a half years to become a Sitecore subsidiary at a $225M price tag on $26M raised.

The next layer — decision-stage measurement, reasoning-chain analytics, the diagnostic-remediation-re-probe loop — is on the same trajectory, and probably on a shorter clock. The infrastructure to measure whether a brand is chosen, not merely cited, exists. Peer-reviewed working papers establishing the methodology — including the Algorithmic Reputation Equivalence framework and the PSOS/CSR architecture — have been on Zenodo since the spring. The question is not whether decision-stage measurement becomes a category. It is which DXPs realize they need it before their customers ask the budget question they cannot currently answer.

The Honeymoon and the Hard Part

Mergers and partnerships in the AEO space are, on balance, a healthy sign. They mean the category is real. They mean enterprise marketers are demanding consolidated tooling. They mean the DXP incumbents have stopped treating AI-mediated discovery as a side project.

But the deals announced so far have, almost without exception, married the easy part of the problem — making content retrievable — to the part the DXPs already owned — making content. The hard part, measuring whether any of it produced a commercial outcome at the decision stage, has not yet had its wedding announcement.

It will.

Search got married to content. Now we wait to see who marries measurement.